Throughout our 40-year history, the firm’s views on inflation, interest rates and corporate profits have been fundamental to shaping our Outlook and investment portfolios. Today, it is our view that the forces of disinflation remain powerful and have important implications for portfolio strategy. We continue to anticipate low interest rates for possibly several more years as the Federal Reserve targets for inflation and unemployment are not likely to be reached until at least 2016. Clearly macro concerns remain; however, there are distinct positive secular and cyclical trends taking place in the US today, and corporate profits, margins and market valuations should be strong for those industries and select companies that are best positioned to benefit.

These positive secular trends, which are important drivers of the Outlook, include:

The dramatic increase in US oil and natural gas production,

The US industrial resurgence, and

The gradual recovery in the housing and automobile industries

As a result of these and other forces, the American economy is once again growing and is perhaps the best-positioned major economy in the developed world today. While the media is beginning to focus on these issues, we believe that their importance to the United States is still greatly underestimated. Among the many ramifications are significant improvement in our balance of payments, a strengthening dollar, a more globally competitive manufacturing base and a reduction in energy imports. These forces have led to a resurgence in America’s industrial competitiveness relative to the rest of the world. Importantly, these conditions foster a low inflation environment which helps keep interest rates low, while benefitting borrowers (homeowners and banks) and the equity markets. Further supporting capital flows to the US are the aggressive monetary policies of Japan and the continued weakness in the European Union brought about by the austerity policies intended to address the debt and deficit problems of member nations.

This Outlook expresses our views of inflation and disinflation, interest rates and the investment implications of these forces. Critical disequilibrium persists in the global economy as evidenced by Europe’s debt, deficits and political challenges, Japan’s attempts to reflate its economy through aggressive monetary policy, North Korea’s nuclear threats, China’s industrialization and evolving phases of growth, the continuing instability in the Middle East and the US government’s deficit and unfunded liability challenges. Nevertheless, we believe that some of the important changes occurring in the United States including the increase in energy production, an industrial resurgence and infrastructure rebuilding opportunities can have a positive impact on corporate earnings growth even as global macro challenges persist, and they will therefore be the focus of this Outlook.

Disinflation and Low Interest Rates Likely to Persist

Fundamental to our Outlook is the likelihood of the persistence of disinflation and low interest rates extending for a considerable period of time. There are many forces in place that should keep inflation (and hence, interest rates) low for several more years, including:

Structural unemployment, which remains a suppressing agent for wages (a key component of the inflation calculation),

Further deleveraging, which retards consumption in a 70% consumer-driven economy,

Inadequate fiscal policy, which is not supportive of growth, and

Quantitative Easing by the Federal Reserve (or purchase of securities by the Fed with newly-printed currency) building up as excess reserves in the banking system rather than flowing through the economy in the form of new loans

To fully appreciate where we are today, it would be helpful to take a brief look back to see how we got here. The severing of the direct convertibility of the US dollar into gold in 1971 kicked off a decade of a falling US dollar and spiraling inflation, characterized by rising energy and commodity costs and further impacted by cost-of-living adjustments in labor contracts and double-digit wage increases. Determined to bring inflation under control, the then Federal Reserve Chairman Paul Volker implemented a tight monetary policy of significantly higher interest rates, which led to a severe recession and record unemployment, but ultimately stabilized the dollar and brought commodity prices and inflation under control. The stronger dollar and stable commodity prices combined with the advent of the outsourcing movement (which put pressure on labor costs) contributed to a secular decline in inflation and interest rates that lasted for nearly 20 years.

The last decade temporarily brought many reflationary forces back to bear on the US. After the US entered multiple wars and expanded its deficit spending, a 10-year bull market for the US dollar came to an end in 2001 and the dollar began a multi-year decline. This occurred at the same time that major population centers such as China, India and Brazil, were achieving critical mass in their rapidly-growing economies and beginning to compete with the developed world for key resources. The combination of a falling US dollar and rising global growth drove oil from a low of $20.00 per barrel in 2002 to a speculative high of over $140.00 per barrel in 2008. It is natural to think of rising commodity prices as “inflationary” however, they can also have a very depressing or deflationary effect on the real economy, especially for an economy such as the US that is 70% consumer-driven. Every dollar spent on foreign imported oil is a dollar not spent productively within the US. One reason the US economy was able to grow during this period is that easing credit terms and new mortgage products allowed consumers to pull equity out of their homes almost like an ATM machine, which led to increased consumption and added an estimated 1.5-2.0% to annual GDP growth, offsetting much of the pressure of high food, gas and heating bills. When the housing bubble burst and consumers could no longer borrow from their homes, the economy entered into steep recession.

Since the financial crisis, the ties between commodity prices and the real economy have been further highlighted. As previously discussed, consumer spending accounts for 70% of US GDP. Today when commodity prices rise and consumers are faced with rising food, gas and heating bills, their ability to spend on other items becomes impaired and they are not able to offset this impairment with additional borrowing. This helps to explain why economic cycles have appeared to be shorter and more volatile since the financial crisis. Each time that oil begins to rise—the real economy begins to slow three to six months later. The deleveraging process of the 1930’s took approximately 12 years to complete, and we expect that the current deleveraging process for many developed nations has several more years to go. Under these conditions, it will be difficult for rising commodity costs to trigger broader inflation until the deleveraging of the developed nations has run its course.

In addition to the shorter economic cycles brought on by fluctuations in commodity prices, another cause of the volatility of the US equity markets in recent years has been attributed to the anticipated withdrawal of monetary support by the Federal Reserve. It is our view that the market is underestimating both the time required to get employment to an acceptable level and the commitment of key members of the Federal Reserve to ensure that the improvement in unemployment is sustainable. Any reduction of monetary policy stimulus under present conditions would be a negative for the economy and for the markets. Therefore, investors should focus on a combination of the inflation rate and the U6 unemployment figures (factoring in labor force participation rates), rather than focus exclusively on the headline U3 unemployment figures. Until such time as the US economy experiences improving employment, there will be little willingness by the Federal Reserve to alter its current policy. Under this scenario, the Federal Reserve becomes less accommodative only when it believes that the economic outlook has already improved to the point that it can withstand the withdrawal of stimulus, which then should not be viewed as negatively by the markets.

Another factor keeping growth contained and inflation low is that the developed world is beset by fiscal austerity when in fact fiscal expansion is necessary to reduce excess capacity and unemployment. Without growth to increase revenues, the ability to reduce debt is much more difficult, further prolonging the deleveraging process. We are seeing attempts to stimulate economies through fiscal policy such as the recently announced $15.5 billion program in South Korea. We are also seeing stimulus attempts through currency devaluation, such as in Japan, although any resulting growth would tend to come at the expense of trading partners, rather than through growing the global economic pie. It is this most unusual combination of forces that shapes our view that disinflation and low interest rates are likely to be in place for several years. If the deflationary forces as described in this Outlook were not so strong, interest rates would not be able to be kept at such low levels by the Federal Reserve. It will be difficult for interest rates to rise while the US economy is awash in corporate cash, tight lending standards exist, consumers are unwilling to increase their debts and students holding loans are in excess of $1 trillion.

One benefit of these disinflationary conditions is that corporations are able to refinance their debt at exceptionally low levels and grow revenues without a commensurate rise in labor costs. As long as the world continues to grow, even at a moderate pace, and while expenses remain controlled, there is a formula for continued profit growth, along with rising dividend payouts. Moreover, the low-growth environment combined with low costs of capital should make corporate restructuring, share buybacks and mergers and acquisitions more attractive and prevalent. On this latter point, as the recovery matures and with corporate cash balances earning virtually nothing, we are seeing boards of directors (partly in reaction to activist shareholders) become more assertive about taking action to see that the valuations of their companies are maximized. We are seeing more companies seeking to unlock value by spinning off or monetizing under-appreciated assets that have not been fairly valued by the market, or undergoing corporate or financial restructuring. Anemic return prospects for bonds should also, on the margin, keep capital flowing into the equity markets, particularly toward those corporations that offer attractive, sustainable and growing dividend yields.

The US Move Toward Energy Independence

Much has been written recently about the potential for the United States to become energy independent after decades of reliance on foreign oil to supplement our own production to meet domestic demand. We believe that the impact of this shift will be more significant than most anticipate.

Many in the energy industry are now predicting that the US may achieve energy independence (or at least North American independence) by 2020 or earlier. This has critical implications not only from a broad economic perspective, but from a geopolitical one as well. The six biggest foreign suppliers of crude oil to the US in 2012 were Canada, Saudi Arabia, Mexico, Venezuela, Iraq and Nigeria. America has seen imports of crude oil decline from a high in 2005 of approximately 10.5 million barrels per day to an estimated 7.6 million barrels a day in February of this year. This decline in imports coincides with an increase in imports in China from 1.2 million barrels a day in 2001 to an estimated 5.5 million in 2012.

Advances in technology have allowed energy producers to extract more oil and natural gas from shale rock more efficiently and cost effectively, allowing older fields that were previously thought to be fully developed to be made highly productive once again. For example, according to the Texas Railroad Commission, the Permian Basin has produced more than 29 billion barrels of oil and 75 trillion cubic feet of natural gas over the last 90 years and was thought to be a mature field. However, the US Department of Energy recently classified this area as the largest producing basin in the United States with up to 30 billion barrels of additional oil. This is only one of many basins in the United States and speaks to the magnitude of the potential to increase production and reserves well into the future.

We have written over the past two years about the political dysfunction in the US and its negative impact on job creation and the economic recovery. One of the most important aspects of the energy opportunity is that those industries that are benefitting are not waiting for the government to fund the necessary infrastructure to make the opportunity become a reality. Aside from the oil and gas producers themselves, other industries that directly benefit include pipeline, storage, processing and transportation companies (rail and trucking), oil services companies and the engineering and construction trades. The state of North Dakota is the poster child for the opportunity with its 3.3% unemployment rate, declining tax rates, increased spending on infrastructure projects (including roads, rails, schools and the electric grid), increased homebuilding and the recent attraction of foreign investment.

According to the Oil & Gas Journal’s latest annual capital spending outlook, energy project spending for this year is estimated to be around $348 billion in the US, and breaks down as follows:

$240 billion for drilling and exploration

$45 billion for production

$13 billion refining and marketing

$38 billion for crude oil, natural gas and product pipelines

It is worth noting that an estimated $38 billion will be spent on pipelines in 2013 which compares with only $8.6 billion spent in 2012. The pipeline construction boom involves spending to build about 4,000 miles of pipeline versus the 830 miles projected for 2012. This is a result of the many recent discoveries and production increases. Furthermore these figures do not include expenditures for additional railroad tank cars to move oil from producing fields to refineries where pipelines do not exist. According to the Association of American Railroads, capital expenditures for railcars is growing rapidly, having increased 46% in 2012 over 2011. At the present time, backlogs are at least two years for railcar manufacturers to deliver the tank cars necessary to transport US crude oil from where it is being found to where it is needed.

The story of the US energy industry is being written every day and the rate of change needs to be fully appreciated in order to properly participate. Client portfolios at ARS are benefitting from the energy and industrial opportunity by owning independent oil and gas producers, refiners, pipeline companies, railroads, as well as companies that provide services to the energy industry.

US Industrial Resurgence

For several quarters we have written about the industrial and manufacturing renaissance that has been occurring as a result of the relatively low energy prices and the growing US competitiveness as wages increase in developing economies, particularly China. One of the byproducts of the US shale revolution has been an abundance of US-sourced natural gas. Unlike oil which can be transported around the globe with relative ease and can therefore trade more or less for a global price, the transportation of natural gas is more complicated. The most common means of natural gas transport is through pipelines, which is only practical for domestic transport. However, to transport overseas, gas must first be super-cooled and liquefied, allowing it to be transported in sufficient quantities by tanker. Presently, there are no permitted export liquefaction terminals in use in the US or Canada, so excess gas is essentially “stranded” resulting in a considerably lower price in the US than in the rest of the world. In fact, US purchasers of natural gas are currently paying approximately $4.00 per mcf, compared with approximately $12.00 per mcf in Europe and $17.00 per mcf in Asia. Although the US and Canada have begun issuing a limited number of liquefaction permits for future gas export, the first terminals are still a few years off, and the US advantaged gas price arbitrage is not expected to close for many years. This has provided an unexpected and material advantage for US-based manufacturers that have a high energy cost component to their production costs. Notable examples include chemical and fertilizer producers, refiners and other energy-intensive manufacturers.

This advantage of low-cost energy is being augmented by a closing of the labor cost gap, as wages in China and other low-cost countries have been increasing at several times the rate of those in the US. China has also begun to get serious about its environmental policy as smog and poor drinking water have rendered some cities close to unlivable and political protests have increased. Enforcement of tighter environmental guidelines also serves to close the cost gap of producing in China. When you combine the lower costs of energy with a diminishing labor and environmental compliance cost advantage and add to that the logistical handicap of needing to ship goods months in advance by containership, it is easy to see how the marginal benefit of offshore manufacturing has declined significantly.

In addition to the slowing of the secular trend of moving production offshore (and in many cases—an outright reversal of that trend), the past two years has also seen the beginning of a cyclical pick up in two of the most important US industries—housing and autos. These two sectors were among the hardest hit during the financial crisis, but several years of below-trend sales has led to low housing inventory levels and older auto fleets. Both sectors have now begun to recover, which should exert a positive influence on the US economy.

America’s industrial resurgence has had the positive impact of strengthening the US dollar. At the same time, the Japanese government has announced a massive program of monetary creation (printing money) to devalue its currency—the Yen—in order improve its global competitiveness by cheapening the cost of its exports. The Bank of Japan’s (BOJ) actions are also designed to encourage consumers to spend to help reflate the economy. Whereas the Yen, the Euro and the dollar have previously been regarded as reserve currencies, the Yen’s role may now be called into question due to its rapid decline. All else being equal, a weakening Yen should have a further strengthening impact on the US dollar. This in turn can have a dampening effect on commodity prices, as most globally-traded commodities are priced in US dollars. Although a strengthening dollar makes US exports less competitive internationally, exports make up only 12% of US GDP, whereas consumer spending makes up approximately 70%. Therefore, a strengthening dollar should have the dual effect of keeping commodity prices under control (the most volatile component of inflation), while also increasing the purchasing power of the US consumer.

The combination of a strengthening currency, an improving economy, low energy costs and generally more competitive production costs is boosting the US economy and making the US among the more attractive countries in the developed world for sourcing new manufacturing operations for a broad range of industries.

The Infrastructure Challenge (and Opportunity)

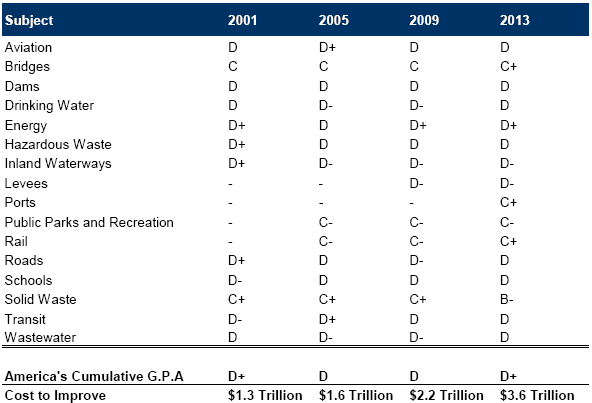

As discussed above, important investments are being made by the energy industry in America’s infrastructure. The need for adequate infrastructure investment is a topic we have written about for many years as it is critical to meet our own societal needs as well as to maintain our competitiveness in an increasingly competitive global economy. Every four years the American Society of Civil Engineers releases its update report on the status of US infrastructure, and once again it is clear how far behind the US has fallen on critical investments in areas such as roads, bridges, rails, power generation and transit. As indicated in the chart below, the cost to improve our infrastructure to a state of good repair has risen from $1.3 trillion in 2001 to $2.2 trillion in 2009 and now that cost has risen to $3.6 trillion in 2013. The report further details that current committed and funded budgets leave a shortfall of $1.6 trillion out of the $3.6 trillion needed to be spent. We are often asked how the US can afford to spend on infrastructure while struggling with record deficits. Some details from the report reveal that continued neglect will cost businesses and households an estimated $1.2 trillion and $601 billion respectively between now and 2020 due to loses from blackouts, brown outs, water main breaks and transit problems. Road congestion alone costs an estimated $101 billion a year to cities. In our view, the more relevant question is how can we afford not to make these investments? The US is estimated to experience 240,000 water main breaks a year. We have over 607,000 bridges with an average age of 42 years, and one in nine is deemed to be structurally deficient. Aside from the economic costs, there are serious safety issues to consider. In 2009, it was suggested that New York City add tidal barriers to its harbor at a cost of approximately $10 to $17 billion. The devastation that Hurricane Sandy inflicted on lower Manhattan came at a far greater cost with some estimates at $50 billion and New York City remains susceptible to another storm.

American Society of Civil Engineers Report 2013

For the world’s largest economy, and one of its most productive, it is imperative that we begin fixing this problem immediately. At a time when reported unemployment stands at 11.7 million people or 7.6%, and total unemployment (U6) is approximately 21.6 million or over 13.8%, fixing our infrastructure will create jobs, increase productivity and enhance corporate profits. Private-sector efforts such as those seen in the energy industry are critical, but government must do its part as well. A D+ grade is simply not acceptable for the world’s leading nation. We continue to watch this area closely, as we believe that signs of a more serious commitment to restoring the US infrastructure would have positive implications for the economy, as well as specific industries that would participate in the rebuilding.

Investment Implications

This Outlook describes an investment environment with clearly-defined opportunities across a broad range of industries and companies at the forefront of a US-based energy and industrial renaissance. Since July of 2012, we have been of the view that the many positives of the US economy were being masked by event-driven or general economic concerns. While we still face many challenges both at home and abroad, this Outlook highlights the abundance of opportunities for investors as is now becoming increasingly evident in the US industrial, basic industry and energy segments of the economy. This is further augmented by the gradual improvement in the housing and automobile markets which have historically been critical to recoveries in the past, and whose benefits have a multiplier effect on the economy. These and other important secular trends discussed in recent Outlooks are driving our thinking on portfolio construction. We continue to emphasize the following areas:

Energy Production and Infrastructure: As described in some detail above, investor portfolios should include exploration and production companies, refiners, pipeline companies, energy servicing businesses and, to some extent, rail and other companies benefitting from increased need for oil transportation.

Beneficiaries of the Revitalization of Industrial America: Areas for consideration include companies benefitting from lower-cost US energy and more generally from the revitalization of US industry, including select railroads, chemical companies and industrials.

Technology and Select Media: Internet traffic continues to swell and is expected to grow by a factor of four in as many years. Mobility, cloud computing, machine-generated information and internet video are among the underlying drivers of internet use. Data center companies and owners of wireless spectrum will be key beneficiaries as businesses and consumers demand access to data anytime and anywhere. We also see opportunities in the media industry with content companies (producers of original programming), benefitting from the emergence of novel distribution outlets. High-quality content owners will benefit from an expanding customer base that can be serviced at negligible incremental costs, positioning them to benefit from the disruptive era in video distribution that is occurring.

Financials: We continue to believe that several leading large-capitalization US financial companies remain under-valued, having still not recovered to the low end of their valuation ranges that they were valued at prior to the financial crisis. These companies are managing to thrive despite a weak interest rate spread environment. They have gained significant market share from second tier and international banks, and have stronger balance sheets than they have had in decades. We are also seeing opportunities for select financials that are direct beneficiaries of the recovery in the US housing sector.

Dividend Growers: With interest rates at historic lows, investors should look to benefit from the attractive dividends currently available from select corporations with strong balance sheets and policies of raising dividend payouts over time. We note that S&P 500 companies have increased dividends each year from $196 billion in 2009 to an estimated $281 billion in 2012 for an increase of 43%. According to S&P data, US companies paid out an additional $14.5 billion in common stock dividends with cash payments increasing 12%. Pay-out ratios remain well below the historic average of 52% and currently stand at 36%. With interest rates expected to remain low as discussed at length in this Outlook, we believe strong business franchises with above-average dividend yields will play an important role in portfolios.

Currency Devaluation: Coming into this year, we felt the environment would be constructive for gold prices. In spite of the recently announced devaluation of the Yen, gold prices for most of the year traded sideways as the dollar strengthened and more opportune equity investments became important competitors for investment dollars. More recently, gold has undergone a dramatic decline. Ironically, the solution to the banking crisis in Cyprus, which would normally make gold more attractive, has raised fears that Cyprus and possibly other central banks might sell gold to reduce debt or make payments. We are mindful of the fact that it was the shift of central banks from being net sellers of gold to net buyers that helped initiate and fuel the bull market in gold of the last decade. Moreover, a stronger US dollar is providing a further near-term headwind for gold. There is also a growing consensus in the markets that quantitative easing is falling short of creating inflation which negates one of the reasons some investors hold gold. Under these circumstances, gold’s intermediate-term outlook has become less clear and we have recently reduced our exposure. Longer term, we remain of the view that the likelihood for continued monetary creation makes gold an attractive alternative currency, and we will look for opportunities to increase exposure in the future, either at lower prices or once we have greater conviction that the current headwinds for gold are subsiding.

Cash: As discussed in previous Outlooks, the excessive debt burdens of developed economies took several years to build up and will not resolve themselves quickly. It is quite possible that the tug-of-war between genuinely positive investment factors and the concerns over slowing global growth and deleveraging, along with greater accompanying volatility, is likely to be with us for some time. At times of higher market complacency and lower margins-of-safety in company valuations, portfolios may temporarily have higher cash balances. At this time, ARS cash positions are being held to be invested in those companies where valuations are approaching attractive margin-of-safety valuation entry points as a result of market volatility