The sharp pullback in U.S. equity prices has created many compelling opportunities for companies we currently own and companies we are considering for inclusion in client portfolios. As our regular readers are aware, historically the months prior to a mid-term election have tended to be volatile and generally negative for stock markets, and the current correction was no exception. However, the period following an election has typically provided strong returns into the end of the year for investors. As we wrote in our September Outlook, stocks trade in an auction market where buyers exchange dollars for shares of businesses. In the recent market pullback, there has been a temporary absence of buyers that has created significant opportunity for long-term investors. Following such periods, premier companies can provide significant returns for investors when buyers return to the market. Given the sudden and sharp move in stock prices, we felt it appropriate to share with you our thoughts on three key questions:

– What drove the market pullback?

– What are we doing as a result?

– What are our highest conviction opportunities going forward?

What drove the market pullback?

As we wrote in our last Outlook, today’s stock market is more short-term oriented than ever before as ETF, algorithmic and high-frequency trading have come to dominate daily trade volumes. The structure of the market has changed with more short-term trading done by computers and algorithms focused primarily on price movements, and not fundamentals. The computer-driven trading trends that drive prices up or down are leading other market participants to react to the price movements exacerbating the price action. Recently, headlines highlighted that the global economy has been slowing somewhat and conditions have become somewhat less favorable due to concerns about companies lowering guidance, trade conflicts, geopolitics (Saudi Arabia, Brazil and Germany), recent comments by Federal Reserve Chairman Powell on future rate hikes, debt, deficits and the China economic slowdown. What is lost in the frenzy of the recent trading activity is the fact that fundamentals remain relatively strong for the U.S. economy and for the businesses at the core of our secular trends – tech, defense, healthcare and select consumer companies as well as small capitalization companies.

Strong balance sheets and free cash flows should matter more than in recent years. It is worth noting that we are experiencing a transition from a liquidity-driven market to a more fundamentally-driven one, which is positive for active management and the many companies we favor whose earnings and free cash flows are expected to grow again in 2019.

What are we doing as a result?

We are making some adjustments to the portfolios, looking for opportunities to reduce taxes by realizing capital losses, and by taking advantage of the opportunities created by the recent pullback by adding to selected positions. Importantly, our secular views remain intact and we are putting cash to work in a measured way. We are focused on positive fundamentals of the businesses we own and other companies whose valuations have become particularly compelling. While the economic headwinds have increased, we maintain our strong conviction in the secular forces that we have identified and the fundamental value of the companies in our portfolios. Howard Marks, a legendary investor, has said that, “Investment success requires sticking with positions made uncomfortable by their variance from popular opinion.” We share his viewpoint, and believe that the short-term price movements do not reflect either the business realities or the fundamental valuations that are inherent in our portfolio holdings, despite the recent sharp declines in stock prices. Doing right in investing often involves doing what is initially unpopular. While more and more market participants are making decisions based primarily on price and popularity, our decisions continue to be business-driven based on our judgment of the outlook for cash flows and earnings growth. In the past two years, we have generally held higher cash levels to take advantage of price dislocations due to the realities of today’s market structure. We are currently redeploying some of that cash by buying companies we believe are on sale.

What are our highest conviction opportunities going forward?

Those companies that are benefitting from the secular trends we have identified for several years should continue to generate higher cash flows and earnings allowing them to continue to invest to increase their competitive positions, raise dividends and repurchase shares. To this end, we continue to focus on the secular trends favoring technology (including cloud, memory, storage, the internet of things), health care, energy, and defense companies among others. Smaller capitalization companies should continue to be attractive given their more domestically-oriented businesses in light of the growing challenges of investing in foreign markets. We believe that many positive factors for U.S. corporations and the U.S. economy continue to be underestimated. By implementing the tax cuts and increased deficit spending in advance of the introduction of tariffs, the Administration has, at least in the near term, offset some of the negative consequences of the changing terms of trade. Moreover the devaluations that are occurring in the emerging market economies have the effect of augmenting the attractiveness of the United States economy and its markets. Notwithstanding the changes to the structure of the market, investors should not underestimate the impact of the powerful technological advances coming over the next 36-48 months that will affect every industry.

If you have any thoughts or questions about our views or your portfolio, please feel free to call us.

“The underlying principles of sound investment should not alter from decade to decade, but the application of these principles must be adapted to significant changes in the financial mechanisms and climate.”

– Benjamin Graham, investor and professor widely acknowledged as the “father of value investing”

We have always viewed the markets as a medium of exchange, swapping dollars for shares of businesses understanding that the opportunity to build long-term capital lies in the discrepancy between the real worth of a business and its stock price as determined by the auction market. Our focus is to own a relatively small number of the best-positioned, best-valued companies in the market, and not the market itself. Investments are made in client portfolios with a view to holding them for the medium to longer-term believing that these companies are the beneficiaries of the secular trends driving the global economy. Before committing capital, our research must produce a clear picture of those investments that are deemed to offer the most cash flow, assets and earnings for the fewest dollars invested. We evaluate a stock the same way we would value the purchase of an entire company. This is the approach we have successfully employed for over 45 years. As more and more market participants make investment decisions based primarily on price and popularity, our decisions continue to be business-driven, based on our judgment of the outlook for the business fundamentals.

While our core principles for investing have not and will not change, the application of those principles must be adapted to changes in the environment as the stock and bond markets today are very different from previous ones. In our April Outlook, we discussed how important convergences in monetary policy, global politics and trade were creating challenging conditions for stock and bond investors. This Outlook will more narrowly focus on some of the key changes that are impacting the structure of the equity market in the United States. These include the significant drop in number of publicly traded companies, the concentration of power of leading corporations, the explosive growth in the number of investment vehicles available and the technological advances such as artificial intelligence, machine learning and high speed trading that are redefining the market’s mechanics and investment approaches. Today’s market is more short-term oriented than ever before. Understanding these changes will enable investors to better navigate the challenges that currently exist and take advantage of opportunities to build and preserve capital. We still believe that many positive factors for U.S. corporations and the U.S. economy continue to be underestimated. In fact, the United States continues to attract significant capital as the currency devaluations that are occurring in the emerging market economies have had the effect of augmenting the attractiveness of the United States economy.

What has changed in the U.S. equity markets?

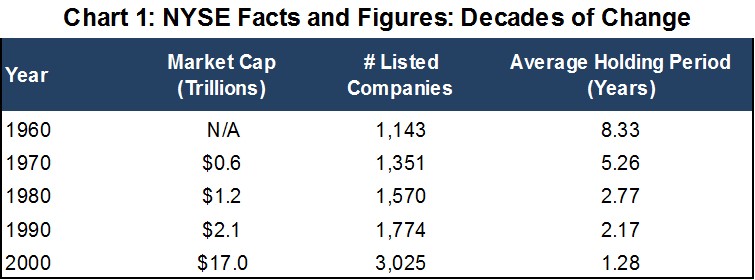

The two most significant changes in the U.S. equity markets are the dramatic drop in the number of publicly-traded companies and the growing concentration in the power of America’s leading companies. These topics were the focus of the recent Jackson Hole Symposium hosted by the Kansas City Federal Reserve. Using the Wilshire 5000 Total Market Index (Wilshire 5000) as a proxy for the U.S. equity market, there were roughly 5000 publicly traded stocks in 1974, a figure which peaked at 7562 in 1998 and has declined to about 3492 companies as of December 31, 2017. According to Wilshire, there have not been 5000 stocks in the index since December of 2005. As shown in Chart 1, a historical review of the New York Stock Exchange (NYSE) confirms a similar pattern with the number of NYSE-listed companies declining to about 2800 as of the end of 2017.

So why has the number of listed companies declined so dramatically? There are two reasons – the low number of newly listed firms and the high number of firms delisting. The lower number of new listings reflects greater opportunity for small businesses to access private capital from either venture capital or private equity investors and the desire for smaller companies to avoid the regulatory burdens of being a publicly-listed company. Bear in mind that private equity firms are sitting with an estimated $1.7 trillion in un-invested capital and continue to raise record amounts of capital. The high number of firms delisting is due, in large part, to the increase in merger and acquisition activity that has been supported by high cash balances at large. corporations, capital repatriation and private equity firm investments supported by the low interest rate policy of the last decade which has made acquisitions highly accretive. In the U.S., there were 5,326 deals in 2017, with a combined value of $1.26 trillion according to a report by Mergermarket. In 2016, there were 5,325 deals, with a combined value of about $1.5 trillion. The United States has accounted for over 40% of global merger and acquisition activity for some time.

“In 1954, the top 60 firms accounted for less than 20% of GDP. Now, just the top 20 firms account for more than 20%.”

–Brookings Institution report by William Galston and Clara Hendrickson

As the number of companies in the public markets has declined over several decades, the concentration of industries has increased. This trend is accelerating as disruptive technologies are affecting companies in all industries. According to a JPMorgan report on global M&A, “technology is creating more differentiation between the largest, most successful firms and the rest of the market, which suggests that disruption is fueling a “winner takes all” environment.” In a working paper by Kathleen Kahle and Rene Stulz titled “Is the U.S. Public Corporation in Trouble?” produced for the National Bureau of Economic Research (NBER), the authors highlight that “In 1975, 50 percent of the total earnings of public firms was earned by the 109 top earning firms; by 2015, the top 30 firms earn 50 percent of the total earnings of the U.S. public firms. Even more striking, in untabulated results we find that the earnings of the top 200 firms by earnings exceed the earnings of all listed firms combined in 2015, which means that the combined earnings of the firms not in the top 200 are negative.” Just look at the technology industry today, where Apple and Google operating systems run nearly 99% of all smart phones. Google and Facebook dominate the mobile advertising market, while Amazon, Microsoft and Alphabet dominate the cloud services business. Amazon is expected to capture almost 50% of the U.S. e-commerce market by the end of 2018. While much has been made about the potential for such concentration of power in the hands of a few with respect inflationary pricing, the history of these firms has been to lower prices by disrupting industries. The dominance of these companies can more likely be attributed to their financial strength, their ability and commitment to invest in research and development, and their willingness to reinvent and reinvest for the future. The combination of their dominance and financial strength are reinforcing the competitive positions of these firms as the rich get richer in corporate America.

How is the investment landscape changing?

Concurrent with the changes in the equity markets, market participants now have more choices than ever to participate through a variety of investment vehicles and investment approaches. According to the Investment Company Institute (ICI), the mutual fund industry in 1960 consisted of 161 U.S.-registered funds totaling $17.03 billion. In 2017, there were over 7,956 U.S-registered mutual funds with 25,112 share classes totaling $18.75 trillion.

The number of Exchange Traded Funds (ETFs) has grown from around 120 in 2003 to more than 1,700 today. While both are baskets of securities, ETFs added a new element to the equity markets in that mutual funds are only priced daily, whereas ETFs are priced and trade continuously like individual stocks. Furthermore, technology is enabling algorithmic trading that utilizes high-powered computers to buy and sell massive amounts of securities in milliseconds. Consequently, high-frequency trading (HFT) allows traders to move in and out of short-term positions at high volumes and high speeds to capture sometimes a fraction of a cent in profit on every trade. HFT is a type of algorithmic trading characterized by high speeds, high turnover rates and extremely short-term investment horizons. Computer-based trading has become a much larger part of the market’s daily activity and focuses almost exclusively on price movements rather than on business fundamentals. It is estimated that computer-driven trading accounts for 80-90% of trading volume daily.

What do these changes mean for investors?

“The single greatest edge an investor can have is a long-term orientation.”

– Seth Klarman, Founder of Baupost Group and legendary hedge fund investor

While it is difficult to ascertain the average holding period for stocks, the figure has declined considerably as shown in Chart 1. The average holding period for an NYSE stock has dropped from 8.3 years in 1960 to an estimated 1.2 years in 2000, and the number is believed to be even lower today. Holding periods for high-frequency-traded securities have been estimated by some sources to be as low as 11 to 22 seconds. Today more securities are traded based on price movements than are bought and sold based on the fundamentals of the underlying businesses. The growing disconnect between price and fundamentals is creating a greater opportunity for longer-term investors.

While these changes are occurring within the structure of the market, the global economy is in the midst of a period of unprecedented monetary and fiscal policy initiatives, growing economic divergences, challenges to the post-WWII global order, and shifting terms of trade. With a dizzying array of investment choices combined with current global economic, social and political characteristics, people can be easily confused. Investors need to make a few fundamental choices to determine the best plan to meet their specific goals. Investors need to choose between a market approach based upon predicting price or an investment approach based upon the evaluation of business fundamentals and the real worth of each business. We believe it is difficult, if not impossible, to attempt to do both. Business ownership has proven throughout history to be the best approach to building capital, but it requires patience and a longer-term perspective.

How is ARS addressing the changes in the structure of the market?

“Investment success requires sticking with positions made uncomfortable by their variance with popular opinion.”

– Howard Marks, co-founder of Oaktree Capital, noted institutional investor and author

While more and more market participants are making decisions based primarily on price and popularity, our decisions continue to be business-driven, based on our judgment of the outlook for cash flow and earnings growth. While our core principles for investing will not change, the application of those principles must always take into account changes in the environment. In the past two years, we have generally held higher cash levels to take advantage of the price dislocations due to the realities of today’s market structure. In several strategies, we have reduced the number of securities held, which in part is a reflection of the concentration of power described above, as fewer businesses have been driving the returns of the broader markets. Notably, we have also taken some profits and generated capital gains for clients as the prices of some businesses had been pushed up in the short-term beyond reasonable levels of valuation. Clients should not view trims of a position as a statement on the long-term outlook for that business, but rather as a reflection of our views of over and under valuation. At the same time, businesses at the intersection of important secular trends may experience periods of underperformance and will require some patience in the face of a lack of popularity in the short term. Investors should not confuse popularity, or lack thereof, with the quality of the business or its outlook. A perfect example of this has been the recent price declines of some of our favorite technology holdings where the fundamental outlooks haven’t changed. As a consequence of owning businesses that can fall out of favor for a period of time, client portfolios may underperform the major market indices for some period. Our concern when a business is underperforming is not its short-term popularity, but rather its ability to continue to execute its business plan, grow its cash flows and earnings effectively, and ultimately realize its value.

In addition to the adjustments we are making to our active strategies, we launched the ARS Focused ETF Strategy in March of 2017. This strategy involves our team constructing portfolios that utilize ETFs to express the views put forth in our Outlooks. The strategy is designed to concentrate our investments in ETFs that provide the greatest exposure to our highest-conviction themes, similar to the exposures that we have in our other active strategies. We are excited about this offering as it provides an efficient way to gain the desired exposures, and allows us to manage client portfolios with lower investment minimums.

Those companies that are benefitting from the secular trends we have identified for several years should continue to generate higher cash flows and earnings allowing them to continue to invest to increase their competitive positions, raise dividends and repurchase shares. To this end, we continue to focus on the secular trends favoring technology, health care, energy and defense companies. Smaller capitalization companies should continue to be attractive given their more domestically-oriented businesses in light of the growing challenges in investing in foreign markets. We continue to believe that many positive factors for U.S. corporations and the U.S. economy continue to be underestimated. By implementing the tax cuts and increased deficit spending in advance of the introduction of tariffs, the Administration has, at least in the near term, offset some of the negative consequences of the changing terms of trade. Moreover the devaluations that are occurring in the emerging market economies have the effect of augmenting the attractiveness of the United States economy and it markets. Notwithstanding the changes to the structure of the market, investors should not underestimate the impact of the powerful technological advances coming over the next 36-48 months that will affect every industry.

Published by the ARS Investment Policy Committee:

Brian Barry, Stephen Burke, Sean Lawless, Jared Levin, Michael Schaenen, Andrew Schmeidler, Arnold Schmeidler, P. Ross Taylor.

The U.S. economy is in the midst of the second longest expansion in its history which is being supported by massive tax cuts, deficit spending, growing capital expenditures and some deregulation. The global economy is experiencing strains that it has not experienced in recent times making the United States economy the prime destination for capital flows resulting in a stronger U.S. dollar. This in turn is placing further strains on dollar debt held by foreigners as well as the earning power of multinational corporations. The United States’ economic advantage is such that some of Wall Street’s leading strategists are suggesting that the expansion could continue into the second half of 2021 or even beyond. At the start of the year, the world economy was experiencing synchronized growth. This is no longer the case. As trade tensions mount, investors should recognize that the United States will be less affected as it is a net importing nation. Notwithstanding today’s headlines, we remain constructive on a narrowing group of U.S. equities based on our positive outlook for their corporate profits. Those companies that are benefitting from the secular trends we have identified for several years should continue to generate higher earnings and cash flows allowing them to continue to invest to increase their competitive positions. Given the current economic outlook, investors should focus more closely on company-specific earnings and events. We expect the market to reassess company valuations, especially for those highly indebted companies that may need to issue additional debt or equity to finance their businesses.

In times of considerable uncertainty, many investors make the mistake of overreacting to short-term conditions and market movements. The growing media attention towards trade wars, political divisiveness and immigration issues have been unsettling for many and serve as a distraction from the positive secular trends driving the global economy. Since the market has not had a significant pullback in some time, it is always possible for the markets to experience one. When and if such a pullback occurs, we will use cash to add to our favorite names. The secular trends favoring technology, defense and health care companies remain intact and smaller capitalization companies should be attractive given their more domestically-oriented businesses. We continue to believe that many positive factors for U.S. corporations and U.S. economy continue to be underestimated.

In this Outlook, we discuss the three main challenges for the global economy, share some insights from some of the leading executives of various industries, address client concerns about inflation, and discuss the investment implications of the adjustments occurring in the global economy.

What’s really behind the trade war?

“The People’s Republic of China (China) has experienced rapid economic growth to become the world’s second largest economy while modernizing its industrial base and moving up the global value chain. However, much of the growth has been achieved in significant part through aggressive acts, policies, and practices that fall outside of global norms and rules (collectively, “economic aggression”). Given the size of China’s economy and the extent of its market-distorting policies, China’s economic aggression now threatens not only the U.S. economy, but also the global economy as a whole.”

Excerpt from the White House Office of Trade and Manufacturing Policy Report, June 2018 on China policies

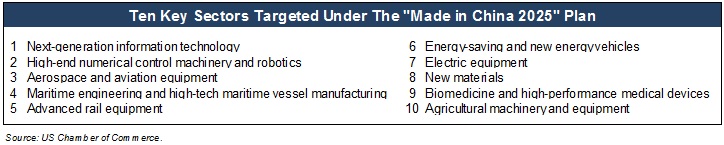

In our April Outlook, we wrote that President Trump was sending a strong message to the world that the U.S. was no longer willing to accept unfair trade practices from any nation. President Trump is following through on his campaign pledge to address unfair trade practices, particularly those of China, which have taken place in a global system to which the World Trade Organization, past U.S. Presidents and other nations have turned a blind eye for decades. In order to change current practices, our trading partners need to be convinced that the U.S. will go all the way in terms of enforcing fair trade. Therefore, suffice it to say that we have now entered into a trade war. The critical underlying issue regarding trade is the battle for future technology supremacy between the United States and China due to economic and security considerations. The concern of the United States is not about competing on the basis of legitimate competitive practices, but rather on China’s use of stolen intellectual property. President Trump’s comments have been directed at China’s “Made in China 2025” plan whereby the Chinese government is supporting what it deems to be strategically vital and important industries in ways that are considered outside of globally accepted practices. The chart on the top of the next page highlights the key sectors being targeted by China according to the US Chamber of Commerce. As we have written for years, data is the new global currency and those that own the intellectual property will have a significant competitive advantage.

As a net importing nation, the U.S. should be hurt less by a trade war than other nations, but there is great uncertainty about the impact of tariffs on global growth. Consumers should expect higher prices on certain goods as many companies will not be able to absorb the costs of tariffs. After a period of strong earnings growth of the S&P 500 companies, we anticipate many companies will be lowering earnings expectations until they have clarity on the impact of changes on their costs and revenues. A trade war at this stage of the global expansion will have repercussions for global growth with Europe and a number of emerging market economies likely being the hardest hit. If this ultimately results in fairer trade and better global security, then everybody wins.

What happens when fiscal and monetary policies clash?

The U.S. tax cuts and higher deficit spending initiatives are requiring the U.S. Treasury to substantially increase the issuance of Treasury securities. Concurrently, the Federal Reserve is attempting to normalize interest rates and reduce its balance sheet. The combination of the clash of the expansion of the federal debt and the contraction of the Federal Reserve’s balance sheet has led to a shortage of U.S. dollar funding which impacts sovereign debt markets and has created a reversal of capital flows. This in turn has reduced the value of emerging market bonds and currencies, and accordingly raised the cost of global commodities traded in dollars. The United States is the world’s largest economy at $19.97 trillion and largest debtor nation at $21.04 trillion with fiscal deficits to be $828 billion estimated for 2018. The U.S. has been running annual trade deficits ranging from $395 billion to $723 billion or roughly 3% of GDP. That our trade deficits are high is well known, but the fact that the trade and fiscal deficits cause the United States to be overly dependent on foreigners to finance fiscal deficits perhaps is not as well understood. The efforts to eliminate unfair trade practices would help reduce our dependence on China and other nations to purchase our Treasuries. While this would have limited impact in the short term, the longer-term benefits would be tangible.

We are monitoring the pace of the rise in U.S. interest rates relative to those of other countries to anticipate future adjustments in currencies and capital flows as well as any debt problems that might arise. We are keeping a close eye on policy changes around the globe to assess their impacts as well. For example, China is in the process of adjusting its monetary and fiscal policies to address its growing debt problems, manage capital flows and its exchange rate, in part to respond to trade issues, and is also considering a proposal to lower taxes to stimulate domestic consumption. Reuters recently reported that the European Central Bank is considering its own version of “operation twist” whereby the ECB will be buying more long-dated bonds next year to keep Eurozone borrowing costs in check even after it stops pumping fresh money into the economy.

So even though it has been 10 years since the debt-induced financial crisis, governments still need to keep borrowing costs down because the recovery needs more time. Perhaps the biggest takeaway regarding interest rates is that investors should expect central banks to feel the need to keep interest rates historically low well into the future. As the economic expansion has progressed, it has not shown itself to be strong enough to withstand higher rates based on the debt burdens facing the global system. Importantly, central banks lack the firepower to respond to the next recession with the traditional tool of significant interest rate cuts. We anticipate this will force bankers to extend the low-interest-rate cycle even beyond current expectations, while on the margin trying to push short rates somewhat higher.

What’s changing in politics today and why does it matter?

“This is an important time in the history of China and the United States as we work our relationship forward … The China-U.S. relationship is one of the most important in the world, [and] must be treasured.”

U.S. Secretary of Defense James Mattis at a 6/26 meeting with President Xi

Three fundamental geopolitical changes we are monitoring are the rise of populism and autocratic regimes in the developed world, the massive migration problem, and the apparent reduction of the United States’ role as the global leader. The United States’ withdrawal from its global leadership role is giving China an opportunity to step up and exert greater influence from an economic and military perspective. At the same time, China’s rise is being augmented by the United States challenging traditional alliances, trading relationships and many of the international institutions that have been in place for over 70 years. China is planning to invest an estimated $1.5 trillion in 80 countries as part of its “One Belt, One Road” initiative that it is using strategically to expand its sphere of influence although the original commitments may be tempered due to concerns about overreach and risks associated with the financing of these initiatives. The geopolitical situation is resulting in an increase in military spending.

The implications of the shifting alliances and anti-immigration sentiment have important ramifications for the future of the European Union and the economic expansion in Europe both of which are quite fragile right now. On the need for European reform, Angela Merkel, Chancellor of Germany, summed up the European challenge with her statement, “if we stand still, we will be pulverized.” On June 28th, European leaders agreed to the framework for an important agreement regarding the migration crisis that has plagued incumbent political parties throughout Europe and threatened to topple Angela Merkel’s coalition government. Given that the deal was put together in an overnight session, many details need to be worked out or this issue will remain politically divisive. Europe still needs to pull together to address the structural issues of the original design of the EU as its governing institutions did not foresee many of today’s key issues. The lack of a common vision is undermining efforts from leaders like France’s Macron to not only increase competitiveness, but to create a compelling and sustainable future for the upcoming generation. Importantly, the majority of people in Europe want to remain in the European Union and we do not anticipate a break up, but the status quo is not sustainable.

What are leaders saying about the economy, trade and secular trends?

We wanted to share some insights from political, business and industry thought leaders to understand their views on the economy, and the secular drivers of growth. The unique perspectives that these leaders bring to the table is invaluable to understand where the world is headed as political and corporate leaders are making decisions for future growth.

On the Economy

Jamie Dimon, CEO of JPMorgan Chase discussing the length of the economic expansion

“I would look at it a little bit more like we’re probably in the sixth inning or something like that … Bad tax policy, bad regulatory policy, bad policies some of which are being fixed and stuff like that. So I think it’s very possible you’re going to see stronger growth in the United States of America and that is picking up a little bit. You see capital expenditures going up a little bit. Consumer and business confidence are close to all-time highs. There are no potholes. I’ve heard [some people] say, well, it’s looking like 2007, completely untrue. There’s much less leverage in the system. The banks are much better capitalized. I can go on and on about the safer system. So, yeah, I think it can easily continue.”

On Trade

U.S.-China Economic and Security Review Commission, 2017 Annual Report, 11/15/17

“The Chinese government is implementing a comprehensive, long-term industrial strategy to ensure its global dominance … Beijing’s ultimate goal is for domestic companies to replace foreign companies as designers and manufacturers of key technology and products first at home, then abroad.”

Brian Coulton, chief economist at Fitch

“A major global tariff shock would have adverse supply side impacts, raising costs for importers and disrupting supply-chains, while reducing consumers’ real wages. The global multiplier effect of lower U.S. imports could be significant. U.S. outward foreign direct investment — the largest source of FDI (foreign direct investment) globally — would probably fall. Along with weaker confidence and lower investment, a global tariff shock would also hit job creation.”

On Technology

George Schultz, a former Secretary of the Treasury, in an Op-Ed in the Wall Street Journal on 6/27/18 on politics and technology

“The world is experiencing change of unprecedented velocity and scope. Governments everywhere must develop strategies to deal with this emerging new world. They should start by studying the forces of technology and demography that are creating it.”

Sanjay Mehrota, President, CEO & Director, Micron Technology from 5/21/18 earnings transcript on the growth of the cloud, data and storage business, and why this technology cycle is different

“One point I would like to make sure that I get across to you is that the cloud, the data center and the intelligent devices on the edge are really forming a virtuous cycle. The intelligent devices rely on more data to provide useful experience but they also create more data that gets stored in the cloud, which makes the cloud bigger, more pools of data created and stored on the cloud and processed in the cloud, that enables cloud to provide even greater value to the edge devices. It unleashes even more innovation and creation of new intelligent devices, more powerful intelligent devices, which then, in turn, guess what, create more data. And so, this is a virtuous cycle between cloud and billions of edge devices really leveraging this data economy to bring great value to the consumers as well as businesses across the globe, and at the heart of this is memory and storage industry and DRAM and flash.”

On Defense

Eric DeMarco, President, Chief Executive Officer & Director, Kratos Defense & Security Solutions, Inc.

“We are seeing significant demand for Kratos‘ target drones in the United States and also globally as a recapitalization of strategic weapon systems to address nation-state adversaries underway. With not only the United States DoD, but every NATO ally increasing its defense spending this year with 15 NATO countries increasing their defense budgets as a percent of their GDP. These strategic systems being deployed need to be exercised against the highest performance and most realistic threat surrogates of the world, which are Kratos‘ targets, and where Kratos is the undisputed an industry leader.”

Should clients be concerned about inflation?

Clients have been expressing concerns about rising inflation. While we acknowledge the near-term inflationary pressures from rising oil prices and tariffs, we believe that longer-term inflation remains constrained by the highly deflationary secular forces of technology, globalization, demographics and debt present in the system. While conditions are right for a modest increase in inflation rates, we do not feel that these concerns are warranted. In fact, the Dallas and Atlanta Federal Reserve Banks held a meeting in May to address this topic and the views are summarized in the quote below from the Dallas Fed. We are focused on the rate of change and will make necessary portfolio adjustments accordingly if inflation rates diverge from our expectations.

“Technology-enabled disruption means workers are increasingly being replaced by technology. It also means that existing business models are being supplanted by new models, often technology-enabled, for more efficiently selling or distributing goods and services. In addition, consumers are increasingly able to use technology to shop for goods and services at lower prices with greater convenience—having the impact of reducing the pricing power of businesses which has, in turn, caused them to further intensify their focus on creating greater operational efficiencies. These trends appear to be accelerating… To deal with disruptive changes and lack of pricing power, many companies are seeking to achieve greater scale economies in order to maintain or improve profit margins. This may help explain the record level of merger and acquisition activity globally over the past few years.”

What are the investment implications?

In our last Outlook, we advised readers that the two quarters preceding mid-term elections have historically proven to be challenging for the markets. The changes in monetary policy, global politics and trade are creating challenging conditions for stock and bond investors. As tempting as it is for investors to be distracted by short-term considerations, we would strongly encourage investors to focus on the secular forces to drive investment decisions. We cannot overemphasize the need to take advantage of the opportunities presented by market pullbacks. The United States should continue to attract capital from the rest of the world which should strengthen the U.S. dollar and constrain interest rate increases. The economic expansion could continue for a few more years and create an opportunity for companies to see even stronger earnings. Central banks will likely conclude that while normalizing policy is a desirable goal, it is secondary to extending the economic cycle for as long as practical in order to delay the next recession for which they do not currently have the tools to effectively address. This means that global interest rates should remain lower for longer than most anticipate. U.S. companies, should continue to enjoy the benefits of massive tax cuts, deficit spending, growing capital expenditures, and some deregulation. However, fewer companies will benefit in the current environment as some could experience supply chain disruptions and higher input costs from tariffs which they may not be able to pass on to consumers. Additionally, the stronger U.S. dollar will reduce earnings for some multi-national companies. As the beneficiaries continue to narrow, the market should react to support the winners at the expense of the rest of the broader market which is highly supportive of active management. Those that benefit from the conditions highlighted above should be well rewarded.

Share prices of some of the leading companies came under pressure in June as profit taking as well as concerns about a trade war had investors selling winners to lock in profits. However, we believe that capital will again flow to companies with above average growth characteristics, strong balance sheets, and high free cash flow to drive investments in future growth. In addition to being big beneficiaries of tax reform and deregulation, small capitalization companies whose earnings are better insulated from tariffs and currency fluctuations offer investors attractive opportunities. We continue to prefer to invest in the areas that are attracting increased capital spending, and those include disruptive technology, defense, healthcare and financial companies. We also favor energy companies in the exploration and production area that have demonstrated greater financial discipline and have become more attuned to purchasing reserves at a discount to market value by using their free cash flows to buy back shares, while benefiting from higher prices. As a result, we have increased our energy exposure this year. We continue to remain cautious on fixed income investments given the risk/reward dynamics and would suggest that investors consider reducing their allocations and shortening their maturities to reduce the risk of capital losses. We recognize that important shifts in the global economy are occurring, and therefore it is a time to be more selective and opportunistic in portfolio construction and asset allocation.

Published by the ARS Investment Policy Committee:

Brian Barry, Stephen Burke, Sean Lawless, Jared Levin, Michael Schaenen, Andrew Schmeidler, Arnold Schmeidler, P. Ross Taylor.

The global economy has again moved into unchartered territory as important convergences in monetary policy, global politics and trade are creating challenging conditions for stock and bond investors. Technological advances and globalization are reshaping politics, economics and society today, and we would caution market participants from relying too heavily on investment experiences of the past to drive investment decisions moving forward. The combination of these forces is also fostering a return to greater market volatility. Over the next few months, market conditions may be unsettled as these changes are absorbed. While the United States and global economies continue their almost decade-long expansions, the U.S. economy is performing marginally less well than expectations which have been quite high following the tax cuts and budget spending increases. As the economy is in the later stages of one of the longest expansionary periods in history, the transition underway will require investors to think differently than they have previously as the current environment is unlike any seen in the past.

Investors should remain focused on their long-term objectives and not allow short-term volatility to cause them to deviate from the path to building and preserving capital. At the same time, investors need to be flexible as the changes occurring in the system will require course adjustments in portfolios to reflect shifting economic realities. Given current uncertainties, the backdrop for investing is somewhat more challenging than when the year began. This Outlook will frame the conditions we expect to be prevalent in the coming quarters and their implications for portfolio strategy. History shows that the two quarters preceding mid-term elections have proved challenging for investors, and we are generally holding higher than normal cash levels to take advantage of the opportunities being created. Importantly, we would remind our readers that the secular drivers for the global economy remain firmly in place and our focus remains squarely on navigating the risks and capturing the opportunities created during this transition. This is to say that those companies benefiting from the secular trends will be the ultimate drivers of capital appreciation, notwithstanding shorter-term pullbacks in their share prices. An important consequence of the changes in the global economy is to anticipate that there could well be fewer winning companies in 2018.

What’s different about this period for stock and bond investors?

The strong equity markets of the past few years have been driven by a synchronized global expansion, strong corporate earnings growth and virtually zero interest rates. Now however, the market is adjusting to a less accommodative Federal Reserve policy, increases in employment and in core inflation as well as potential changes in the terms of global trade. While corporate profits should continue to be robust and grow over the next few quarters, subtle changes in expectations for higher interest and inflation rates could lead to a contraction of P/E (price/earnings) multiples creating greater differentiation in stock market valuations and pressure on bond prices. Following a prolonged period of declining unemployment rates, the large labor pool is now disappearing and creating labor shortages in some industries thereby fostering wage inflation. As the Federal Reserve continues its transition from its zero-interest rate policy to a more normalized rate structure, higher interest rates will create new pressures on highly indebted companies as they will face increasing debt servicing costs. Furthermore, attempts by the Trump Administration to improve what it considers to be highly unfair trade practices have the potential to push up the cost of imports for certain companies, including many that are unable pass these costs along to consumers in the form of higher prices. These circumstances suggest that some companies that previously had been considered safe investments in difficult markets may not provide the same protection that they might have in the past. In this environment, those companies without strong balance sheets to continue to invest and/or meet debt servicing obligations, as well as those lacking the ability to increase prices, improve margins or market share, will be penalized. To offset P/E contraction, companies must be able to grow revenues and earnings, while increasing free cash flow to be able to reinvest for the future of their businesses.

For bond market participants, the situation could well be even more challenging. The bull market in bonds that started over 35 years ago may well have come to an end. To provide some perspective as to how the rate structure has changed, we remind investors that in 1981 the prime lending rate reached 20.5%, money market rates 21%, and the 10-year treasury yielded 15.5%. Today those numbers are 4.75% for the prime rate, 1.5% for money markets and the 10-year is around 2.80%. Presently, the Federal Reserve is targeting 3-4 increases annually for 2018 and 2019 in the Federal Funds rate, while contracting its balance sheet which has grown from $925 billion to $4.5 trillion over the past decade. This is the first time in history that rate increases and balance sheet contraction have occurred simultaneously. Based on these conditions, investors in bond funds may experience losses not consistent with the return experience of the past. Clearly, the risk dynamics of the market are shifting given the changes in the environment. Strategies that worked in the past decade will be unlikely to produce the same results going forward. Investors should be flexible in their approach to portfolio strategy as subtle changes may result in bigger risks as well as bigger opportunities.

Why are politics today so different?

“Not only have we failed to sell globalization well, we also didn’t take care of those who have been affected in the transition to a more global economy. There are many people who have been affected by technological change and globalization who don’t have a clear way to reinvent themselves. So there are tragic cases in many parts of the world – people in broad sections of society who are not able to find a job. So even though I don’t doubt the benefits of globalization, in implementing the liberalization process, we didn’t pay enough attention to these negative side effects of globalization. And now, they’re hounding us.”

– Agustin Carstens, General Manager, Bank of International Settlements

Technological advances and globalization have contributed significantly to the populist movement as shifting fortunes have left many in the developed world worse off than before, while almost 3 billion people in the developing economies have seen living standards rise. The rise of populism has established political parties losing elections to anti-establishment parties or individuals whose main appeal is that they are not the incumbents. The result of these and other concerns has been a less stable geopolitical situation. Social and economic issues are creating a more divisive and polarized political environment in Europe and at home. The populist movement is also encouraging a disquieting rise of autocratic leaders as shown by the recent election of nationalist Viktor Orban as President of Hungary. Since this trend is not limited to just one NATO member, it could have important implications down the road. In addition, the U.S. voter base is more divided than it has been for some time. With big money supporting both parties, the upcoming mid-term elections will create added uncertainty. Perhaps the best example of today’s political climate is in the United States with the election of President Trump. Whether you like him or not, President Trump’s understanding of the frustrations of many Americans who felt victimized by globalization helped galvanize his voter base. So far, his policy initiatives on foreign policy, immigration, taxes and trade have closely followed his campaign platform and investors should expect that to continue. President Trump’s “America First” policy platform and unorthodox approach to governance have kept both allies and enemies off balance. It will be fascinating to watch how efforts to denuclearize North Korea unfold, but the Administration’s approach has created a move to negotiations as the effects of harsh sanctions have taken hold. At the same time that America is stepping back from its role on the global stage, China’s President Xi is aggressively expanding China’s role as a global economic and military power. China has been the biggest contributor to global GDP growth for over a decade and is now exerting its economic and military strength in Asia and beyond by offering developing nations a model for growth that is different than the Western model of democracy and market economics. China is also providing other countries significant investment capital to modernize infrastructure through its “One Belt, One Road” initiative. The contrast in political and economic approaches has the potential to create an even more divisive geopolitical world order. It is not hard to envision a less stable world unless the U.S. and China find a way to lead by partnering going forward. One can also imagine a win-win from the political perspective for both President Trump and President Xi whereby each saves face, but where China’s most significant unfair trade practices would have been successfully addressed. Investors should not lose sight of the fact that China has embarked on a long-term, multi-decade economic and scientific transformation that will not be derailed by trade negotiations with the United States or anyone else.

Why are the terms of trade changing?

We support free trade, but it needs to be fair and it needs to be reciprocal because in the end unfair trade undermines us all. The United States will no longer turn a blind eye to unfair economic practices including massive intellectual property theft, industrial subsidies, and pervasive state-led economic planning. These and other predatory behaviors are distorting the global markets and harming businesses and workers not just in the U.S. but around the globe. Just like we expect the leaders of other countries to protect their interests, as president of the United States, I will always protect the interests of our country, our companies, and our workers.”

– PresidentTrump, excerpts from his speech at the World Economic Forum in Davos

Tariffs, trade negotiations and protectionism have been major topics in the media and on Twitter. As the rate of change continues to accelerate, governments need to be more proactive to maintain global competitiveness and address the needs of those affected more so than they have been in the past. In his Davos comments, President Trump was sending a strong message about the unwillingness of the U.S. to accept unfair trade practices from any nation. The Administration started with discussions with Mexico and Canada on the fairness of NAFTA terms and followed with proposed tariffs to address long-term concerns relating to the steel and aluminum industries. However, the underlying issue regarding trade is the battle for future technology supremacy between the United States and China. President Trump’s comments were a direct shot at China’s “Made in China 2025” plan whereby the government is supporting strategically vital and important industries with low-cost loans and other subsidies. As we have written about for years, data is the new global currency and those that own the intellectual property in technology will have a significant competitive advantage especially with the introduction of the newest technologies such as AI, robotics, blockchain and 5G. As negotiations get underway, both governments are stating that they are complying with the World Trade Organization’s (WTO) trade practices, that neither wants a trade war, and that each will defend its rights.

Technological advances have been reducing the cost of doing business among nations while helping companies set up global value chains with suppliers in many countries. For example, Boeing, the largest U.S. exporter, employs more than 140,000 people in more than 65 countries. In addition, it leverages the talents of skilled people working for Boeing suppliers worldwide, including 1.3 million people at 13,600 U.S. companies. And this is just one company. What would the figures be for all U.S. companies? Global supply chains are a reflection of the interconnectivity and interdependencies of the global economy as well as the cost effectiveness of the global trading system. Therefore the risks of policy missteps with respect to global trade are causing concern among investors. While we do not expect negotiations to escalate into a trade war, the changes in terms of trade will impact industries and businesses differently with some benefiting, some losing and some experiencing minimal impact.

What are the investment implications?

We encourage investors to recognize that what worked in the past may not work going forward as this environment is unlike any other. Fewer companies will benefit, and the market will react to support those companies at the expense of the rest of the broader market. Those that benefit from the conditions highlighted above should be rewarded with premium valuations. Capital has been flowing to the defense, technology and healthcare companies, and we expect those flows to continue, if not accelerate. Interestingly, companies attempting to fight pricing and margin pressures will likely increase their technology spend in an effort to counter those pressures. Despite the likelihood of increasing government regulation, taxation from Europe and scrutiny, technology companies should continue to benefit as increased spending is virtually a requirement for companies to maintain competitiveness as the Internet of Things (IoT) becomes more widely adopted and the industry moves closer to the introduction of 5G. Our emphasis remains on selecting companies benefiting from disruptive technologies, rising defense spending, changes in the financial and healthcare industries, increasing U.S. consumer spending and the shift to a more service-oriented global economy led by China and India. Unlike in the past, energy companies in the exploration and production area have demonstrated greater financial discipline and have become more attuned to purchasing reserves at a discount to market value by using their free cash flow to buy back shares. As a result, we have increased our energy exposure this year. Companies with strong balance sheets that can aggressively invest in the future growth of their businesses should be more highly rewarded as will those with the ability to repatriate large overseas cash balances. U.S. small capitalization companies, which in some cases are more insulated from changes in trade, also stand to be significant beneficiaries of tax reform, strong consumer spending and increases in capital expenditures. We continue to remain cautious on fixed income investments given the risk/reward dynamics and would suggest that investors consider reducing their allocations and shortening their maturities to reduce the risk of capital losses.

At the start of the year, investor sentiment was positive as the global expansion was intact, the outlook for corporate profits remained strong with expectations for interest and inflation rates to rise modestly. As the second quarter begins, the shifts in monetary policy, global politics and trade are creating different conditions for stock and bond investors. Looking at the risks and opportunities stemming from these changes, we anticipate that the second and third quarters will see increased volatility and a narrowing of investment opportunities. With respect to monetary policy, it is expected that the Federal Reserve will maintain its plan to raise rates two or three more times this year and up to four times next year, while also reducing its balance sheet. The mid-term elections in the U.S. may weigh on market sentiment and increase volatility. While it is too soon to determine the outcome of trade discussions with Mexico, Canada and China, changes in the terms of trade could impact global supply chains which may upset the synchronized economic expansion that has been helping drive equity markets. In the near term, changes in terms of trade may lead to higher import costs which would be a negative for the consumer-driven U.S. economy. The nation imports approximately $600 billion more goods and services than it exports each year. Industries that are targets of these changes could undergo a retrenchment as excess capacity may be shut down and short-term supply challenges may result which could drive up prices in this adjustment phase. Since the U.S. has many of the world’s largest companies with sophisticated global supply-chain networks, these companies could experience near-term disruptions in their businesses.

Two other prominent features of the global stock markets have been the surge in Mergers & Acquisitions and the $800 billion in buybacks estimated to occur this year compared to $500 billion in 2017. M&A and buybacks are reducing the number of publicly traded companies and the outstanding shares available to public market investors. This continues to favorably change the supply and demand dynamics for equity ownership. In the past two months, we have been adjusting portfolios to reflect the changes in the environment as we were trimming some holdings, eliminating others, and investing the proceeds in companies with lower P/E multiples as these should perform better during a period of multiple contraction. Importantly, we would remind our readers that the secular drivers for the global economy remain firmly in place, and our focus remains squarely on navigating the risks and capturing the opportunities. For our regular readers, we have not changed our fundamental views on the economy but recognize that important shifts are occurring, and therefore it is a time to be more selective and opportunistic in portfolio construction and asset allocation.

Consistent with past actions, Congress has once again taken the easy path while leaving others the hard work of addressing our nation’s long-term fiscal problems. The passage of a bipartisan federal budget by the Senate and the House, which followed the massive tax cuts passed in 2017, represents an inflection point for U.S. fiscal policy, and one which has important implications for stock and bond market investors. The current concerns about growing deficits and national debt levels are pushing interest rates higher, yet only somewhat higher than the recent historic lows. At the same time, markets are experiencing greater volatility after an extended period of extremely low volatility. Due to the increase in the federal budget deficit, we are modestly adjusting our expectations for interest rates, inflation rates and market volatility, but we are not changing our positive views on corporate earnings and the companies benefitting from this environment. We remain focused on the secular beneficiaries we have defined previously and would remind our readers that the drivers for these businesses remain firmly in place, notwithstanding these changed fiscal and monetary conditions. Moving forward, investors should expect even greater capital flows to the beneficiaries of this Outlook, particularly leading defense, technology and healthcare companies as well as those benefitting from increases in consumer spending globally. One important consequence of the changes in our Outlook is that we anticipate that there may be fewer winning companies in 2018.

Will Corporate Earnings Continue to Rise in 2018?

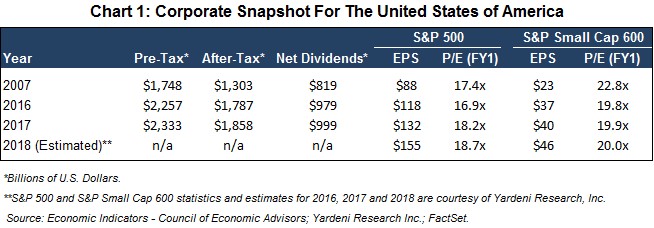

As we wrote in our January 31st Outlook, “we expect corporate profits to increase supported by a synchronized global economic expansion with subdued inflation… this market rise is being driven by rising corporate earnings rather than just an expansion of price/earnings (P/E) multiples which often is a characteristic of the later stages of a market advance.” This view remains unchanged. However, there are two key questions for investors to consider following the tax cuts and increased deficit spending, these are – will the benefits be short-lived and how broadly will they benefit companies? The recent pullback notwithstanding, we believe that 2018 and likely 2019 will see a continuation of the growth in pre-tax and after-tax profits (as highlighted in Chart 1), but that the changes in fiscal and monetary policies will create an unequal playing field for U.S. corporations and small businesses. Well-respected investment strategist Ed Yardeni, of Yardeni Research, Inc., forecasts S&P 500 earnings of $155 in 2018 and $166 in 2019. Yardeni Research projects the S&P 500 will reach 3100 by the end of the year which is up from 2726 as of the time of this writing, and that target is based on the belief that the forward P/E will be 18.7. We have followed Ed’s work for some time, and he has been very effective defining the environment for many years. We expect that those businesses with strong balance sheets, the ability to raise prices, invest aggressively to offset inflationary pressures and increase productivity will be rewarded, and those that cannot will be penalized. Ironically for businesses, the budget deal adds additional near-term fiscal stimulus, and increased deficit spending will increase demand which should further boost corporate earnings.

What are the Pros and Cons of the Recently Approved Budget?

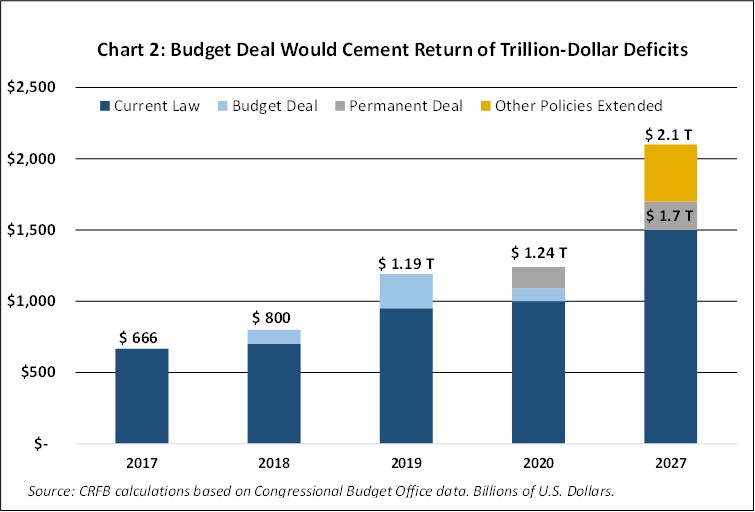

The budget deal is one with a few near-term positives and many longer-term negatives. On the positive side, the Senate and House are significantly boosting defense spending after years of underinvestment following sequestration. This spending increase comes at a critical time as our military needs to upgrade, replace and modernize to maintain its strength. The challenges of sequestration were evident in the deadly naval accidents that have occurred in recent years. In short, the U.S. was putting the brave men and women of our armed services at greater risk than necessary. These multi-year spending increases are meaningful in a world where the geopolitical picture remains unstable with potential troubles looming with Russia, North Korea, China and the Middle East. Some needed domestic social programs also received additional funds including the Children’s Health Insurance Program. Additionally, the budget suspends the debt ceiling until March of 2019 so that neither party can hold the nation hostage for political gain until then. On the negative side, The Committee for a Responsible Federal Budget (CRFB) estimates that the budget increases will add $300-400 billion to the deficit and possibly add more than $1.5 trillion of new debt over the next decade. According to the CRFB press release, “this deal represents budgeting at its worst – each party is giving the other its wish list with all the bells and whistles included and asking future generations to pick up the tab.” The CRFB estimates have the federal deficit rising from roughly $665 billion in 2017 to projected $1.2 trillion dollars in 2019 and over a trillion dollars for the foreseeable future as shown in the Chart 2.

One of the critical issues facing investors is the inherent conflict between this expansionary fiscal policy and the Federal Reserve’s efforts to normalize monetary policy by raising interest rates and reducing its balance sheet. This is happening while leadership of the Federal Reserve is transitioning from Janet Yellen to Jerome Powell. In response to this concern, Treasury yields (which had been gradually rising for two years) have moved up more aggressively over the past eight weeks rising nearly half of a percentage point on the 10-year Treasury bond. We will be closely monitoring the rate of change of Treasury yields, the foreign exchange value of the dollar, and the appetite of buyers to purchase the new supply of Treasuries that is required to fund the growing federal deficit. Conversely, we would not be surprised if interest rates stall or move down to the lower end of the trading range in the near term, as rapid changes are often met with counter-trend moves. With the national debt forecast to rise to $21.5 trillion this year and the economy in its best position to continue its expansion since the financial crisis, this is not an ideal time for the government to be adding more stimulus to the economy. Unfortunately, our elected officials have “kicked the can down the road” once again by not addressing entitlements in this process and by not allocating the proper spending to infrastructure needs which require over $4.6 trillion just to maintain the system in a state of good repair. We believe many of our infrastructure needs can no longer be postponed, and state finances are such that they cannot be relied on to foot a significant portion of the bill. This would argue for even higher deficits in the years to come as the inevitable infrastructure problems will need to be financed through additional deficit spending by the federal government.

Quick Thoughts on Active versus Passive Management, Leveraged Products and Derivatives

“The inherent irony of the efficient market theory is that the more people believe in it and correspondingly shun active management, the more inefficient the market is likely to become.”

– Seth Klarman, founder of the Baupost Group

Many investors have moved to passive investing through mutual funds or exchange traded funds (ETFs) based on the belief that markets are efficient. We do not share that belief as our philosophy has always been that securities trade in an auction market with inherent inefficiencies. The market volatility of the past few weeks provided a reminder that passive investing assures investors that they participate fully in the markets’ returns achieving both 100% of the upside and 100% of the downside in the market moves. Given that we are at an inflection point in policy, this sets the stage for a narrowing of opportunities and a more favorable backdrop for active management. Therefore, we believe that investors taking a passive approach should consider increasing the actively-managed portion of their portfolios. As a reminder to our readers of the dangers of leveraged products and the use of derivatives, we would point to the $2.2 billion Credit Suisse low-volatility product that recently lost 96% of its value overnight and is now being closed.

Investment Implications of the Outlook

“The only other thing I’d say is that too many investors look at the present. The present is already in the price. You have to think out of the box and sort of visualize eighteen to twenty four months from now what the world is going to be and what securities might trade at. What a company’s been earning doesn’t mean anything. What you have to look at is what people think it’s going to earn. If you can see something in two years is going to be entirely different than the conventional wisdom, that’s how you make money.”

– Stanley Druckenmiller, legendary investor, speaking at the USC Marshall School of Business

This is an interesting time for investors as the contemporaneous shifts in U.S. fiscal and monetary policy regimes, occurring at a later stage in the business cycle, will have important implications for investment strategy. We believe that the ability to distinguish between the companies that benefit from rising deficits, higher interest rates and modest inflationary pressures, from those that get hurt, is going to be critical for investors. Historically markets eventually come under pressure during periods of rising interest rates, but within the market not all companies are treated equally. We strongly believe that fewer companies will benefit from this environment, and that the market will react to support those companies at the expense of the rest of the broader market. Those that benefit from the conditions highlighted above will be rewarded with premium valuations. Capital is already flowing to the defense, the technology and the healthcare companies, and we expect those flows to continue and possibly accelerate. Interestingly, companies attempting to fight inflationary pressures will likely add further to their technology spend in an effort to counter those pressures. Our emphasis remains on selecting companies benefiting from disruptive technologies, rising defense spending, changes in the financial and healthcare industries, increasing U.S. consumer spending and the shift to a more service-oriented global economy led by China and India. Companies with strong balance sheets that can more aggressively invest in the future growth of their businesses should be more highly rewarded as will those with the ability to repatriate large overseas cash balances. U.S. small capitalization companies also stand to be significant beneficiaries of further improvements in the economy, tax reform, strong consumer spending and increases in capital expenditures. We continue to remain cautious on fixed income investments given the risk/reward dynamics, and would suggest that investors consider reducing their allocations and shortening their maturities to reduce the risk of capital losses.

While we remain positive on the outlook for corporate earnings to rise and the continuation of the synchronized expansion of the global economy for 2018, we must keep in mind the risks present in the system that can impact longer-term investment strategies. In the coming months, one risk we will closely monitor will be the rate and magnitude of change in interest rates. We described many of these risks in detail in our December 2017 Outlook. Businesses that are proactively investing to redefine themselves will have a chance to compete, while those that do not will be left behind.

For our regular readers, we have not changed our fundamental views on the economy but recognize that an important shift in fiscal policy has occurred, and therefore it is a time to be even more selective and opportunistic in portfolio construction and asset allocation.

The rising equity market is being met with a level of skepticism from the average investor that would normally be associated with a much less positive economic backdrop. Given the many concerns we have heard expressed about valuations and elevated market levels, we thought it would be appropriate to share a brief note to discuss why we expect the market advance to continue, notwithstanding the potential for a pullback at any time. In this Outlook, we share our thoughts on why investors are so skeptical, why the market appreciation should continue, and how investors should position themselves to benefit. For our regular readers it is worth noting that the positive views for 2018 as expressed in our 2017 Outlooks have not changed and in fact have been reinforced. We expect corporate profits to increase supported by a synchronized global economic expansion with subdued inflation. It is particularly noteworthy that this market rise is being driven by rising corporate earnings rather than just an expansion of price/earnings (P/E) multiples which often is a characteristic of the later stages of a market advance.

Why are investors so skeptical?

“In times of rapid change, experience could be your worst enemy.”

– J. Paul Getty

While a healthy dose of skepticism is always appropriate when investing, the post-financial crisis period has created an economic and market environment with little or no historical precedent and one which has been confusing for investors. Yet most investors rely on past experiences and historical references to reinforce their views, positive or negative, of the current situation as hindsight provides the highest level of clarity. While we also use our past experiences to frame our views, we believe that the distinct characteristics of the current environment make historical comparisons less relevant. At the same time, we fully appreciate the factors that have made it difficult for market participants to feel confident. Below we highlight some of the key issues weighing on investor sentiment and distracting investors from the many opportunities being presented today.

Globalization and Technological Advances – the rate and magnitude of change brought about by globalization and technological advances is so great that most market participants are challenged to adapt, and these changes are requiring more rapid adjustments in the global system. For many, keeping up with the rate of change is overwhelming.

Geopolitical Dynamics – The unconventional political setting is challenging the norms, fueling populism and nationalistic sentiment. Political dysfunction and frustration with the flawed efforts of governing institutions are all too common themes in many developed nations pressuring existing political parties to reassess their platforms. Many find this environment unsettling and some believe it has to end badly for the West, the country and the market.

Social Concerns – The uneven distribution of the benefits of the economic recovery has resulted in growing income inequality and education/skills gaps globally. This type of wealth disparity fosters growing social unrest. As technology displaces old industry jobs, older workers are being increasingly challenged to adjust. This is occurring as the United States is reaching full employment and as the developed economies are seeing unemployment rates decline as well.

Unconventional Monetary Policy – Following the most accommodative period in its history, the Federal Reserve is attempting to normalize monetary policy by gradually raising interest rates and shrinking its balance sheet. Given the historically low level of interest rates and limited room for central banks to stimulate economic activity if needed, they must put themselves in a position to effectively respond to a future recession. Therefore central bankers in working towards normalization must, at the same time, be careful to extend the business cycle. This will also buy time to reduce national debt as a percentage of GDP.

Why should the market appreciation continue?

“This game of economic miracles is in its early innings. Americans will benefit from far more and better ‘stuff’ in the future. The challenge will be to have this bounty deliver a better life to the disrupted as well as to the disrupters.”

– Warren Buffett, as reported in Newsweek, 1/5/18

The strong market appreciation in 2017 that continued in January of this year can be attributed to two main factors – accelerating corporate earnings growth and a synchronized global economic expansion that has been stronger than many anticipated. Bear in mind that an earnings-driven market typically reflects a stronger economy and therefore is on sounder footing than a P/E-driven market. The corporate earnings outlook is being further supported by repatriation of cash held overseas and in some cases lower regulatory burdens. This is occurring even before the much-needed investment in infrastructure has been made. Corporate earnings and global growth are benefiting from several factors including:

Pent-up Demand – One of the consequences of the financial crisis was that deleveraging became a priority over consumption and capital spending. We are now seeing pent-up demand translate into higher spending by both consumers and businesses thereby increasing overall economic activity.

Unprecedented Monetary Policy Support – Although monetary policy in the developed world has begun to tighten, it remains accommodative by historical standards. While gradually lessening, the accommodative monetary conditions should remain in place for an extended period.

U.S. Tax Cuts – The tax changes, with accelerated depreciation for capital spending, are positive for earnings and economic activity in the U.S. and abroad. Moreover one aspect of the new tax rules that is not getting as much attention from equity investors is that the changes to interest deductions should push companies that can to reduce debt, strengthen their balance sheets and increase equity values. Unfortunately, not all companies will have the financial wherewithal to reduce their debt burdens and will lose some of the benefits of interest deductibility. This will set up a key point of differentiation among businesses in the next 12-24 months.

Technology – Companies are taking advantage of technology to grow more efficiently. It is enabling companies to do more with less, reduce input costs and focus on productive growth.

How should investors position portfolios to benefit?

“The rate of change has never been this fast, and yet will never be this slow again.”

– Justin Trudeau, Canadian Prime Minister in his Davos speech.