Central banks have been responding to an accident-prone and fragile global economy with the most accommodative monetary policy structure in history and are likely to continue this approach for some time. However, monetary policy has its limits and market participants are becoming increasingly concerned that we may be approaching those limits. The resulting uncertainty and volatility have led to distortions in the prices of businesses which create opportunities for patient, long-term investors. This is a good time for investors to have higher cash balances, not as a market call, but rather to be in a position to take advantage of the opportunities presented. Because this is not an environment where all businesses perform equally, actively managed portfolios should benefit. The United States has been the primary beneficiary of this environment among leading economies. As the largest economy in the world and a safe haven, the United States has been attracting significant capital flows as it is the most important, resilient and adaptive of all the major economies. The U.S. is gradually improving in measures of industrial activity, employment, wages, housing, consumer net worth and consumer confidence. However, despite these improvements the Federal Reserve recently declined to raise interest rates even a quarter of a point citing the weak overall global backdrop. This continuation of record low interest rates for the past eight years should be proof enough that monetary policy alone cannot deliver sustainable growth without fiscal policy initiatives which are now needed to support more balanced growth. For investors waiting for a normalization of interest rates, the wait will continue to be long as it requires a return to “normal” economic conditions which cannot occur under present circumstances.

The goal of each Outlook is to define the supply and demand dynamics of economies to understand global capital flows and the prospects for interest rates, inflation rates and corporate profits which are fundamental to security valuation. There are many forces causing shifts in these dynamics including, but not limited to, currency changes, economic divergences, and migration stemming from political upheaval. For example, China’s currency devaluation on August 11th increased concerns about further competitive devaluations, deflationary pressures and slowing global growth. These conditions have created growing imbalances and increased strains as a consequence of slowing growth and rising debt levels. For much of the past 20 years, global growth was primarily driven by China’s rapid expansion that pulled along many emerging and commodity-producing nations. Now those same nations are suffering as export-driven and debt-fueled growth has slowed precipitously, and the world economy is now experiencing a reversal of fortune as evidenced by the massive capital outflows from these nations to the United States and select European countries. Based on the current Outlook, expect to see a continuation of low interest rates, low inflation rates and slowing growth. The environment remains positive for the U.S. economy, while slowing global growth is placing a premium on those United States and European companies that can maintain their own growth dynamics.

“The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.”

Federal Reserve Press Release, September 17, 2015

After nearly eight years of historically low interest rates, the Federal Reserve Open Market Committee (FOMC) on September 17th voted to maintain its current interest rate policy. The strength of the United States economy is challenging the Federal Reserve to balance a modest interest rate increase against the unknown impact of China’s slowdown on global growth and the impact of a rate increase in draining additional capital from struggling emerging economies. The U.S. continues to demonstrate positive, but muted growth. In addition as one of the largest consumers of energy, U.S. consumers and corporations continue to receive a windfall in the form of lower energy prices which acts as a form of economic stimulus. Unlike any other major economy, the United States benefits from the current global dislocations and China’s slowdown, but only up to a point. The economy, while improving, is not immune to the challenges facing the world, and we cannot be the sole engine of global growth. Raising interest rates at the same time other nations have weakened their currencies puts upward pressure on the U.S. dollar which results in our $2.8 trillion of imported goods and services coming in at lower prices and augmenting deflationary pressures.

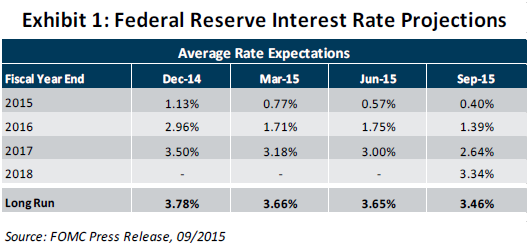

Prior to the FOMC meeting, both the International Monetary Fund (IMF) and the World Bank voiced concerns that a rate increase by the FOMC would accelerate capital outflows from weakening emerging market nations – something they can ill afford. While a 0.25% increase in short-term rates should not have had much of an impact on the United States economy, the decision to delay the initial rate increase speaks volumes about the fragility of the world economy. Exhibit 1 represents the lowering of the FOMC’s average rate expectations from December 2014 to this month. It suggests that regardless of the timing of a rate increase, the U.S. will experience abnormally low interest rates well into the future.

“China, whose currency is tied to a rising U.S. dollar making its exports more expensive, is becoming less competitive at a time when it needs to increase exports to slow its decline in GDP growth to a more manageable level. If the U.S. dollar remains strong, China may find it necessary to devalue its currency to support its exports. A strong dollar also has important implications for the global bond market as there is more than $9.2 trillion of dollar-denominated debt held by foreigners.”

The Outlook, April 9, 2015

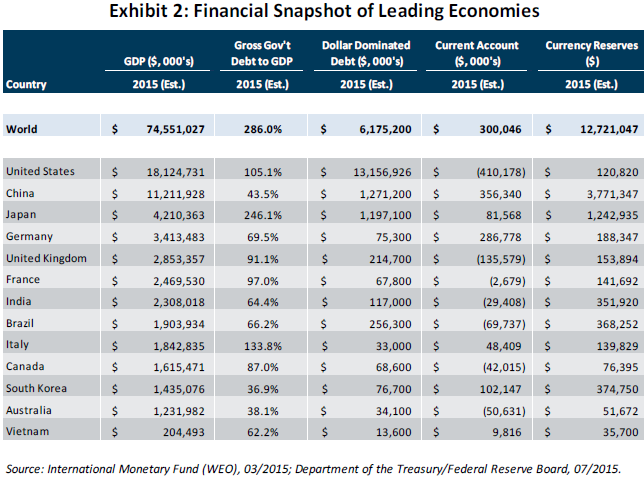

While the U.S. stands out among the major economies, China, Europe, Japan and the emerging nations reflect the divergences we have written about for some time. The uniqueness of the challenges facing each requires the use of different applications of currency, monetary and fiscal policy to return to sustainable growth. As monetary policy tools are closer to their limits, policy makers have been using currency devaluation in attempting to support their economies. As illustrated in Exhibit 2, these nations are not all equally equipped to attack the problems given their respective debts, currency reserves and trade balances. The emerging economies are suffering from their reliance on China and struggling under debt burdens that accumulated during the China-led boom. After attracting capital for many years, these countries are now experiencing a reversal of capital flows, rising debt servicing costs (as much of the debt is tied to a rising U.S. dollar), increasing inflationary pressures, political and social stresses. The combination of the above is driving capital to the United States adding to fears that capital outflows can accelerate when the Federal Reserve actually raises interest rates.

The move by the People’s Bank of China (PBOC) to devalue its currency was a direct response to weaker July export data for the world’s largest exporter. The move was in recognition of the fact that China could not and should not have its currency so tightly linked to a strengthening U.S. dollar which would make Chinese exports more expensive at a time when its economy has slowed from over 10% GDP growth for most of the last 20 years to 7% recently according to the government. China is more likely growing at 5% or less as the government statistics are questionable at best. No export-driven country should have its currency linked to a strong or rising currency if it wishes to protect its export business.

While China is dealing with some economic difficulties at this time, it has the fiscal and monetary resources to manage through these or at the very least to minimize them. As highlighted in Exhibit 2, China has an estimated trade surplus of more than $350 billion. It also has currency reserves of roughly $3.8 trillion, including $1.2 trillion in U.S. Treasuries. From a monetary policy perspective, China has room for further interest rate cuts to stimulate growth. In the past, the government also has demonstrated a willingness to use large-scale fiscal policy initiatives and may very well use this approach again if necessary. While the last big fiscal stimulus initiative in 2009 helped the global economy, it sowed the seeds for some of China’s current difficulties because many projects were perhaps not such productive investments. Nevertheless China has the resources and the will to support its economic growth in contrast to other countries with the resources but not the will.

Recently China has been aggressively establishing itself as a military, political and economic power on the global stage. It has aspirations for a more dominant role in the world from both an economic and political perspective. It is China’s goal to become an IMF member, to have reserve currency status, and to exert its influence on the world monetary stage. The recent actions to manage its stock market have set it back from achieving these goals. Clearly China is struggling as an economy in transition, but it has a long-term plan that it is pursuing, a growing middle class and an ability to learn and adapt. With the need to create over 10 million new jobs a year to maintain social stability, it should be expected that the government will do whatever it feels is necessary and leave the market to play its role at a later date. Investors should bear in mind that China is playing the long game in its economic development.

Europe has been experiencing more positive but muted economic growth following the temporary resolution to the Greek debt crisis. Based on the improving but fragile state of the European economy, President Mario Draghi announced on September 3rd that the European Central Bank (ECB) stood ready to extend, if necessary, its monetary program to stimulate the European economy especially if current developments in emerging market economies negatively impacted the region’s trade and confidence. However, Europe is now facing another test from the growing refugee crisis. With the ongoing civil war in Syria, the emergence of the Islamic State (ISIS) and the continued instability and poverty, refugees are fleeing the Mideast and North Africa to the shores of Greece, Italy and Turkey in overwhelming numbers. Not only is it likely that the ECB will need to extend its quantitative easing program and low interest rate policy, it has been necessary for fiscal policy initiatives to be implemented to accommodate the influx of refugees.

The migration crisis poses a multi-dimensional problem for governments in Europe. First, there exists a climate of resentment from those nations that have been forced to implement austerity programs, and are now being asked to accept a portion of refugees by the same countries that imposed the austerity in the first place. Second, there are increased social strains of providing basic essentials to the refugees. Nationalist parties are using xenophobic rhetoric to gain political support among those opposing the resettlement of the refugees. Europe overall has a 12.2% unemployment rate with much higher youth unemployment. In some countries the influx will create further resentment and social challenges in the nearer term. Longer term, there is the potential positive impact from the refugees as most should eventually become valuable additions to Europe which has been facing a long-term demographic problem that these people would help offset. For example, Germany has a 4.6% unemployment rate and as many as 1.1 million job openings. At the present time, these refugees need food, housing, medical services and jobs in order to become productive members of society. All this comes at a cost which suggests that the ECB monetary policy program will need to be augmented by stronger fiscal policy.

Today volatility has increased in all markets due, in part, to the dislocations we are experiencing in the global economy. There are other factors impacting volatility as well. First, the global economy is progressively more accident-prone and fragile as it remains stressed by high debt levels and slowing growth. Second is the post-crisis regulatory regime that requires financial institutions to hold higher levels of capital and make changes to their business models which have resulted in a reduction of capital market liquidity. Many of the regulations enacted since 2008 were designed to prevent a recurrence of the financial crisis, but do not address the current and future needs of the capital markets. Additionally, the structure of the market has changed with high frequency traders (HFTs) and exchange traded funds (ETFs) playing a bigger role in trading activity. To take advantage of the resulting price distortions of securities in the markets, client portfolios are generally holding higher cash positions to move quickly as opportunities are presented. The U.S. economy continues to do well, but we may decide to increase the cash position further if conditions in the emerging markets continue to deteriorate and spill over into the U.S. In recent months, we eliminated from client portfolios any bond positions deemed to be less liquid or potentially vulnerable credits and replaced with high grade investments.

As discussed in our recent Outlooks, the current global economic and geopolitical dynamics strongly suggest a continuation of low interest rates, low inflation rates and slowing growth for the foreseeable future as the global economy cannot tolerate a normalization of interest rates under the present conditions. To repeat, investors waiting for a normalization of interest rates, the wait can be long as it requires a return to normal economic conditions which cannot occur under present circumstances. The United States remains the standout economy, and we should continue to see moderate improvement in economic activity. Under present conditions, areas of focus include:

As always there are risks to our investment Outlook that we factor into our views. We view the remainder of 2015 as an environment which will favor active management and domestically oriented companies. Our research continues to identify strong businesses that are well positioned to benefit from the conditions described. Client portfolios reflect companies with the following characteristics: improving margins, increasing free cash flows, ability to increase pricing power, market share gainers and growing dividends. In a low-growth environment, expect the market to continue to assign premium valuations to high-growth companies due to the scarcity value.

Sign up to receive The Outlook — our timely newsletter featuring our investment and economic thinking — and highlights from our latest market insights will be emailed directly to your inbox.

All investing involves risk, including the potential loss of principal.

© 2025 ARS Investment Partners, LLC