In this issue:

The character of the post-crisis US economy augers well for a period of continued low growth, low inflation, low interest rates and rising corporate profits. One of the reasons this period has been so challenging for investors is that we are operating in an economic and investment environment that is unprecedented. While certain characteristics of this period are reminiscent of those past, there are critical differences as well. Few investors have operated in an environment that enjoyed the prospects for reaccelerating US manufacturing growth along with expectations of continued low inflation and near zero interest rates for a sustained period of time. The political dysfunction in Washington highlighted by the debt and deficit debate will likely continue to be a major distraction for investors until a long-term solution is established, but investors who take a longer-term view should be well rewarded.

The US economy is slowly but steadily improving, and that is more important in our view than the distractions often written about in the news media. New technology in energy exploration and recovery along with decelerating growth in emerging markets is relieving pressure on commodity prices and providing an important stimulus for the US economy which is more than 70% consumer-spending driven. This stimulus (in the form of lower gas prices and moderating food and heating bill inflation), along with low interest rates, is making homes and automobiles more affordable and tempering the negative headwind of consumer deleveraging that has been occurring since the financial crisis. Lower energy costs are also making US manufacturers more cost-competitive and stimulating new manufacturing investment.

At the same time, structural headwinds discussed in this Outlook are keeping unemployment stubbornly high which is suppressing wage increases. The combination of stable-to-falling commodity prices with stagnant wage rates is keeping overall inflation low and allowing the Federal Reserve to maintain its current accommodative monetary policy. Most economic cycles are ended when rising inflation prompts central banks to raise interest rates to slow growth. However, we expect low inflation to stay in effect for some time, creating the prospect for a prolonged economic expansion, albeit with lower growth than we were accustomed to in prior decades. It is the unusual combination of these economic factors that make this cycle unique.

Many might assume that structural headwinds to more rapid economic growth would be negative for stocks because of reduced prospects for revenue growth. However, a climate of low but steady growth, but also low inflation and lower interest rates (in contrast to shorter cycles of “boom and bust”) can, in fact, be favorable for equity markets, leading to gradual multiple expansion where investors are willing to pay higher prices for a given company’s earnings, cash flow and assets. This is particularly true in light of the relatively less attractive comparable offerings in cash and fixed income.

The Federal Reserve is likely to remain a major force in defining the current environment. This view was reinforced by the recent nomination of Janet Yellen to become the next Chairwoman of the Federal Reserve. The post-crisis policies of the Federal Reserve have been in reaction to and in anticipation of the structural impediments, and investors should expect Ms. Yellen to maintain a highly accommodative stance for as long as necessary for the Federal Reserve to meet its dual mandate of full employment and price stability.

Several structural headwinds are likely to prevent the US from achieving the 3-4% real growth rates experienced in the 1980’s and 1990’s, including high unemployment, wage stagnation and the need for consumers to deleverage. While many will view these impediments as negatives for the market, the environment remains a positive one for equity investing, as described in this Outlook. The following is a review of the key structural impediments facing the US today.

High Unemployment and Labor Market Issues

The US is experiencing chronic unemployment partially hidden by declining labor market participation rates and made worse by technology-driven productivity improvements. This is a far more complex problem than the US Bureau of Labor Statistics’ (BLS) reported unemployment rate (known as U3) of 7.2% or 11.3 million people out of work would indicate. An example of the degree of the problem is that long-term unemployed (those jobless for 27 weeks or more) stands at 4.1 million persons or 36.9% of the unemployed. The U3 measurement of unemployment understates the magnitude of the problem since it does not count those who have stopped looking for jobs as well as those forced to work part-time rather than full-time. The broader measure, known as the U6 unemployment rate, totals more than 20 million people or 13.6%.

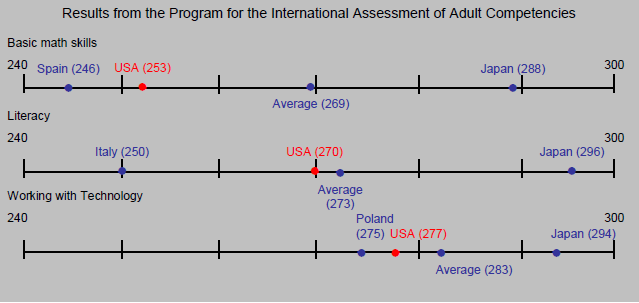

A fundamental issue is the mismatch between the skills needed for available positions and the skills available in the labor pool. According to a new report by the Organization for Economic Cooperation and Development (OECD), the skill level of the American labor force has fallen dangerously behind its peers based on assessments of literacy, math skills and problem-solving. The US needs to refocus its education system on the skills required to reduce the current level of unemployment.

Source: National Center for Education Statistics, “Literacy, Numeracy and Problem Solving in Technology-Rich Environments among U.S. Adults.”

Other factors are also impacting the employment market, including the inability for US workers to move easily to other areas for a new job. This had historically been a key advantage for the US in previous recoveries, but the collapse in the housing market made it more difficult for many workers to move to find employment because they were unable to sell their homes. Moreover, many companies were reluctant to hire new workers due to uncertainty regarding tax and fiscal policies. Given the present rate of new job creation, it could take years to resolve the problem and return to acceptable employment levels. The Federal Open Market Committee (FOMC) recently forecast that job creation would remain challenged, as the committee members are estimating it will take until the end of 2016 for the U3 unemployment number to return to a more normalized range of 5.2-5.9%, and this anemic rate of job creation could weigh heavily on Federal Reserve policy for a considerable period.

Wage Stagnation Issues

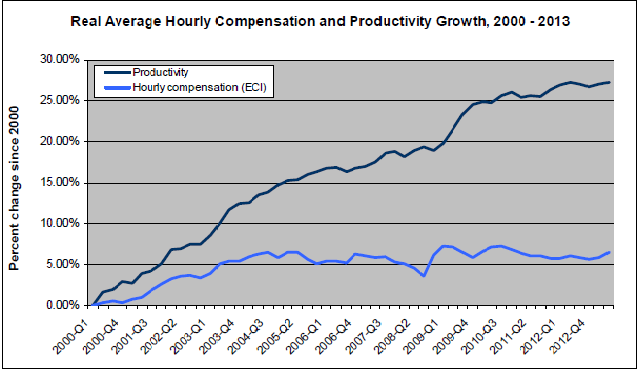

Further compounding the growth problem is the fact, that for most of the American population, wages have not grown in the past decade. According to the Economic Policy Institute, during the period of 2002-2012 “the vast majority of wage earners has already experienced a lost decade, one where real wages were either flat or in decline.” In fact, the real average hourly wages of workers with a college degree were lower in 2012 than they were in 2002 according to the BLS, and the college wage premium (the amount by which wages of college graduates exceed those of high school graduates) narrowed considerably.

As we head into November, we are constructive on the potential for equity returns driven by price earnings multiple expansion resulting from the distinct characteristics of the prolonged, low-growth business cycle described in this Outlook. This view is further supported by other positive factors for corporations including record corporate profits, fortress balance sheets and increasing cash flows as well as corporate activity including mergers & acquisitions, share repurchases, and dividend increases. Due to some of the uncertainties surrounding the dynamics of the global economy and long term US fiscal and tax policy, corporations are generally investing cash for the most certain shorter-term economic results rather than investing where future uncertainties make commitments more difficult. Taken in the aggregate, these factors create a favorable environment for equity selection as a combination of low interest rates and low inflation levels will tend to drive higher valuations for businesses with strong and stable growth characteristics. The outlook for anemic yields on cash and fixed income investments presents a compelling case for capital to flow into equities.

Based on this Outlook, we are constructive on the equity markets and in particular on the following themes: America’s industrial and manufacturing resurgence; energy companies and the beneficiaries of the US shale gas development; the evolution of media consumption and the importance of proprietary content; growth in mobility and data; the financial, housing and auto recovery; companies with attractive and growing dividends; and companies with special situations or company-specific drivers. Due in part to the challenges of the global economy, US small and mid-capitalization stocks have been strong performers and are attracting continued interest as they often derive most of their revenues from within the US. While the global economy is also in a low growth mode, those US companies with strong earnings growth should continue to be well rewarded.

Sign up to receive The Outlook — our timely newsletter featuring our investment and economic thinking — and highlights from our latest market insights will be emailed directly to your inbox.

All investing involves risk, including the potential loss of principal.

© 2025 ARS Investment Partners, LLC